Singapore’s approach to supporting micro, small, and medium enterprises (MSMEs) blends targeted grants, risk‑shared loans, and advisory services anchored by Enterprise Singapore (EnterpriseSG) and partner agencies like IMDA and SkillsFuture. Rather than one “silver bullet,” the system is a toolkit that MSMEs can assemble to match their growth stage—starting up, digitising core operations, deepening capabilities, and expanding abroad. This article maps the major policies and funding programmes and how they fit together, so founders and managers can see the path from idea to internationalisation.

At the capability‑building core is the Enterprise Development Grant (EDG), which co‑funds projects in three broad thrusts: upgrading core capabilities (strategy, branding, HR, finance), innovation and productivity (process redesign, automation), and market access (internationalisation work streams). Projects are typically delivered by qualified consultants or solution providers, with outcomes such as revised business models, streamlined workflows, or new customer acquisition channels. The Productivity Solutions Grant (PSG) complements EDG by subsidising pre‑approved, off‑the‑shelf digital and equipment solutions—think accounting, e‑commerce, CRM, HRIS, and POS—curated under IMDA’s SMEs Go Digital. PSG is designed for fast adoption; EDG is for deeper, bespoke transformation.

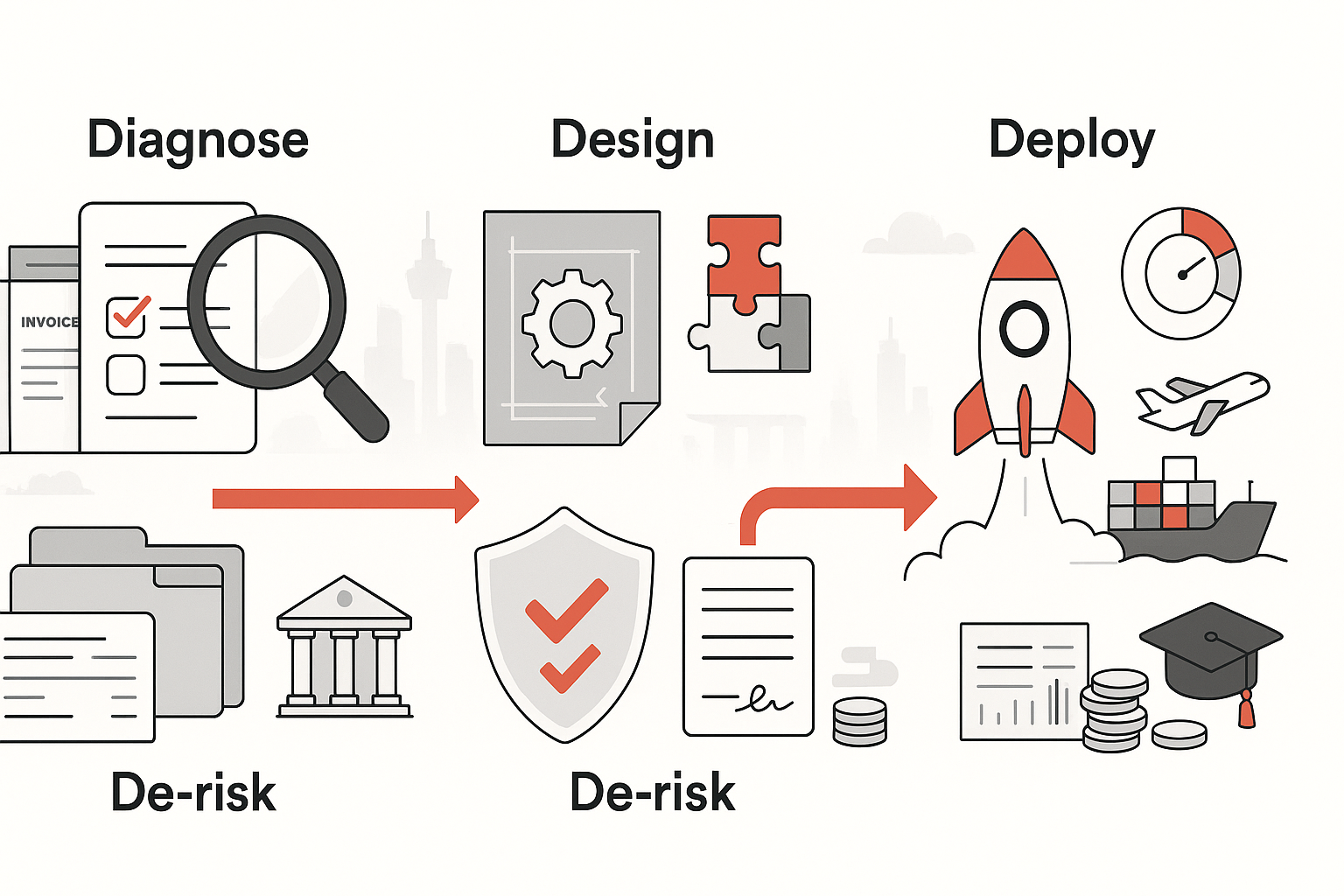

To reach customers overseas, the Market Readiness Assistance (MRA) grant helps defray eligible costs for activities like overseas marketing, business matching, and participation in trade fairs. For capital needs, the Enterprise Financing Scheme (EFS) works through participating financial institutions, with the government sharing a substantial portion of default risk. EFS has variants for working capital, trade financing, fixed assets, project loans, and venture debt—useful at different points in the business lifecycle. Early‑stage founders can also look to the Startup SG umbrella (e.g., Founder, Tech, Equity), which mixes grants, mentorship, and co‑investment to catalyse innovation‑led ventures.

Beyond cash and credit, policy support includes advisory and one‑stop navigation. SME Centres offer free business diagnosis and guidance on suitable schemes, while the GoBusiness and GovAssist portals simplify discovery and application. IMDA’s CTO‑as‑a‑Service and Start Digital packages help firms identify the right stack and onboard with minimal friction. SkillsFuture complements the above with course subsidies and the SkillsFuture Enterprise Credit (SFEC) to co‑fund enterprise‑level transformation and training.

Eligibility commonly hinges on being a Singapore‑registered entity with meaningful local shareholding and meeting SME thresholds (e.g., group revenue and headcount bands). Many grants require applications to be approved before committing to vendors, and firms should budget for outcome tracking and, where relevant, third‑party audits. Strong applications articulate problems, quantify benefits, specify deliverables and timelines, and show management commitment (resources, team, milestones). Banks will expect cash‑flow projections and collateral details for loans, even under EFS.

Smart sequencing helps: adopt PSG solutions to stabilise operations, use EDG to redesign processes and build capabilities, tap MRA to enter priority markets, and layer EFS loans to fund working capital and assets. Avoid double‑claiming the same cost under different grants, maintain clean procurement and timesheet records, and keep an eye on scheme refreshes announced in the annual Budget. Programme parameters evolve; always verify current details with EnterpriseSG, IMDA, and participating banks.